Abstract After experiencing the urgency of the fourth quarter of 2016 and the turmoil of the first quarter of 2017, the RMB exchange rate has come out of a painful winter and returns to the long-term track of stable operation. In view of this, we judge that the renminbi will become a "new normal"...

After experiencing the urgency of the fourth quarter of 2016 and the turmoil of the first quarter of 2017, the RMB exchange rate has come out of a painful winter and returns to the long-term track of stable operation. In view of this, we judge that the renminbi will become a "new normal", and the relatively comfortable exchange rate operation is expected to continue for a long time, thereby consolidating and promoting the internationalization of the renminbi. "Tianshi personnel day reminder, the winter solstice Yang Shengchun came again." Since March this year, the exchange rate of the renminbi against the US dollar has risen steadily, and the consensus at the beginning of the year has gradually disappeared. So, is this stability a short-lived accident, or is it a medium- and long-term trend? We believe that the three key pillars of the stability of the RMB exchange rate have quietly formed, laying the foundation for the long-term trend to stabilize.

From the internal factors, the expected management at the beginning of this year not only effectively broke the devaluation consensus, but also formed a long-term restraint on the depreciation of the depreciation; from the external perspective, due to the end of the "Trump market" of the US dollar, the RMB exchange rate operation situation improved, and the exchange rate policy got rid of From a fundamental point of view, the "811" exchange reform has so far, the release of the RMB effective exchange rate overvaluation pressure has been completed in stages, and the introduction of the countercyclical factor in the RMB intermediate price formation mechanism is just the right time.

With the above pillars, after experiencing the urgency of the fourth quarter of 2016 and the first quarter of 2017, the RMB exchange rate has come out of a painful winter and returns to the long-term track of stable operation. In view of this, we judge that the renminbi will become a "new normal", and the relatively comfortable exchange rate operation is expected to continue for a long time, thereby consolidating and promoting the internationalization of the renminbi.

Expected management to defeat the devalued demons. In October 2016, the irrational depreciation of the renminbi was gradually becoming a mystery, triggering a rapid depreciation of the renminbi against the US dollar for several months and creating heavy pressure for capital outflows. At the beginning of 2017, Chinese regulators seized key opportunities and broke the depreciation consensus with the expected management of diversification. It formed a continuous suppression of the depreciation and created a suitable market atmosphere for the RMB exchange rate to stabilize.

Expected management to grasp key opportunities. From December 2016 to January 2017, the market formed a consensus on excessive concentration of RMB, so a small reversal force at the margin could trigger a chain effect. At the same time, the liquidity of the overseas RMB market was extremely tight, and the cost of shorting the RMB was greatly increased, which aggravated the market reaction after the trend. Seizing this opportunity, Chinese regulators have intensively introduced a series of measures to enhance the expected management of the RMB. Affected by this, in January 2017, the RMB exchange rate against the US dollar rebounded strongly. The onshore and offshore prices accumulated 715 and 1187 basis points in the month, triggering the market to step on the market and defeating the RMB depreciation.

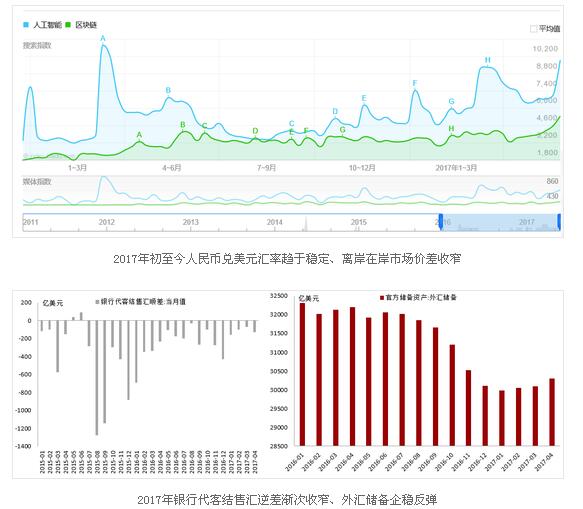

The devaluation of the demons is continuously suppressed. This round of expected management not only gave birth to the renminbi's opening, but also formed long-term suppression of irrational devaluation expectations. Since February 2017, the onshore and offshore exchange rates of the RMB against the US dollar have not only operated steadily, but the price difference between the two has been positive from 2016 to negative and has been narrowed (see the attached picture). ). This shows that the original RMB depreciation consensus has basically been resolved, and market expectations are returning to rationality. As market expectations improve, the pressure on capital outflows has also eased significantly. Since January 2017, the bank's settlement of foreign exchange settlement has gradually narrowed, and the scale of foreign exchange reserves has reached a three-month rebound after bottoming out (see photo).

The exchange rate operating situation is ushered in a change. Since March 2017, the US dollar index has continued to fall, and the RMB exchange rate has shifted from scenario C to scenario B. Thanks to this, the two bottom lines of the RMB exchange rate policy are no longer under pressure at the same time, and the dilemma of the central bank's policy choices has gradually disappeared, thus providing continuous guarantee for the stable operation of the RMB exchange rate.

The policy dilemma is over. As pointed out in our previous report, after the “811†exchange rate reform, the short-term operation of the RMB exchange rate can be divided into scenario A, scenario B and scenario C (see the attached figure for details). Since October 2016, the situation C has not retreated. The US dollar index continued to rise, and the two bottom lines of the RMB exchange rate policy were simultaneously under pressure, causing the central bank to fall into a painful dilemma: Tolerating the rapid depreciation of the RMB against the US dollar may lead to an unexpected loss of control. Strengthening the strengthening of the RMB against the US dollar will amplify the extent to which the RMB deviates from the long-term equilibrium. . This dilemma forced the exchange rate policy to carry out a complex dynamic balance, which is the key cause of the cold winter of the RMB exchange rate. Since March this year, the US dollar index has dropped from the high point of 102.1 to around 97, pushing the situation C to change to scenario B. The long and tormented policy dilemma is over.

Happy time is expected to continue. With the dust of the French elections set, the risk appetite in the European market was boosted, and the exchange rates of the euro and the British pound against the US dollar bottomed out. On the other hand, Trump's "leakage door" triggered a continuous crisis of trust, and the delay of large-scale fiscal stimulus will suppress the dollar's trend for a long time. Therefore, the US dollar index will continue to decline with a high probability, and thereafter remain at a low level, and the RMB exchange rate operation will also be located in Scenario B and Scenario A for a long time. Under Scenario B, as the US dollar index is lower, it is only necessary to maintain the staged stability of the RMB against the US dollar, so as to slow down the overvaluation pressure of the effective exchange rate of the RMB. Under scenario A, since the US dollar index is stable at a non-absolute high, the gradual and orderly depreciation of the RMB against the US dollar can achieve a sustained release of the RMB effective exchange rate overvaluation pressure. In view of this, in the next few months, the two bottom lines of the exchange rate policy will remain stable, the central bank's decision-making will get rid of the dilemma, and the RMB exchange rate operation will usher in a long-term and pleasant phase.

The overestimation of pressure release is nearing completion. The renminbi currency is the currency map of China's economic fundamentals. The equilibrium exchange rate based on fundamentals is the core representation of the bottom line. Drawing on relevant academic research [1][2][3], we constructed an econometric model based on BEER theory and measured the RMB equilibrium exchange rate (see the attached figure for details). The calculation results show that since the "811" exchange reform, the release of the RMB effective exchange rate overvaluation pressure has been completed in stages, and the RMB fundamentals will strongly support the stable operation of the exchange rate:

First, the “811†exchange rate reform effectively releases overestimated pressure. During the period of 2014Q3-2015Q2, the real effective exchange rate of the RMB was higher than the equilibrium exchange rate for a long time, and the difference between the two was gradually expanded, indicating that the overvaluation of the effective exchange rate of the RMB became increasingly serious at this stage. During the period of 2015Q3-2016Q3, the difference between the real effective exchange rate of the RMB and the equilibrium exchange rate gradually narrowed until it almost disappeared. This shows that after the “811†exchange rate reform, the two-way floating and flexible exchange rate operation mechanism based on market supply and demand has achieved initial results. Under this mechanism, the phased depreciation of the renminbi effectively relieved the overestimation pressure and promoted the internal and external equilibrium of the Chinese economy.

Second, the devaluation of the devil has caused the RMB exchange rate to overshoot. In October 2016, the IMF lowered the forecast of economic growth in the United States and developed countries in the same year, with a drop of 0.6 and 0.2 percentage points respectively, while maintaining affirmation of China's economic growth. Thanks to the comparative advantage of economic fundamentals, the RMB equilibrium exchange rate showed a strong rebound in the fourth quarter of 2016. However, the real effective exchange rate of the renminbi during the same period was significantly lower than the equilibrium exchange rate, and the degree of deviation between the two increased to -1.5%, which formed a serious undervaluation of the renminbi. According to this, the rapid depreciation of the exchange rate of RMB against the US dollar, which began in October 2016, and the sudden increase in capital outflow pressures are all over-regulated by the irrational market dominated by depreciation, which seriously deviates from the objective economic reality.

Third, the overestimation of pressure release has been phased out. In the first quarter of 2017, the real effective exchange rate of the RMB and the equilibrium exchange rate were highly close, and the former was only 0.2% lower than the latter. It can be verified that the expected management at the beginning of the year effectively suppressed the devaluation and quickly corrected the irrational undervaluation of the renminbi. At the same time, the fact that the real effective exchange rate is slightly lower than the equilibrium exchange rate also reasonably explains the steady increase of the RMB exchange rate against the US dollar since April 2017. So far, the pressure of RMB overestimation accumulated before the “811†exchange rate reform has been completely released. Looking into the future, with the changes in China's economic fundamentals and the global economic situation, the relative real and negative exchange rate of the RMB and the relative exchange rate will continue to evolve, leading to two-way fluctuations in the value of the renminbi, but the material basis for long-term, large-value depreciation does not exist. Exchange rate stability has been consolidated.

Fourth, the introduction of the countercyclical factor is just the right time. From the perspective of policy costs, as the current exchange rate operation stabilizes and the overestimation of pressure is released, the introduction of a countercyclical factor in the formation mechanism of the RMB middle price can achieve a smooth and orderly mechanism adjustment and avoid a drastic institutional impact on the market. . From the perspective of policy benefits, after the long adjustment of the "811" exchange rate reform, the effective exchange rate of the RMB has basically matched the equilibrium exchange rate. At this time, the introduction of the countercyclical factor can prevent procyclical fluctuations and further expand the currency miscalculation, so that the effective exchange rate and the equilibrium exchange rate The deviation is maintained within a reasonable range. Therefore, this measure is not only expected to enhance the institutional basis of the stability of the RMB exchange rate, but will further promote the exchange rate to adjust the functional standard of the internal and external equilibrium of the Chinese economy.

references:

[1] Wang Bin. The measurement of the real effective exchange rate of the RMB equilibrium and the exchange rate imbalance [R]. Working paper of the People's Bank of China, October 24, 2014.

[2] Jiang Boke, Li Tiandong. A new perspective of the RMB equilibrium exchange rate theory and its significance [J]. International Finance Research, 2006 (4): 60-66.

[3] Zhang Xiaopu. The theory and model of RMB equilibrium exchange rate [J]. Economic Research, 1999, 12: 70-77.

(The author of this article: Director of ICBC International Research, Chief Economist. The research areas are global macro, China's macro and financial markets.)

Best Tea Infuser,Tea Infuser Teapot,Green Tea Infuser,Glass Teapot With Infuser

YANGJIANG VOSSEN INDUSTRY AND TRADE CO.,LTD , https://www.cnvossen.com