Summary of the current Chinese economic data, although not so pessimistic in July, but the policy is difficult to continue to overweight, there will be more stimulus occurs, it is expected that by the end of the macroeconomic indicators may be difficult to see improvement, to prevent asset bubbles task remains Heavier. Exploring China's economic data...

Although China's current economic data is not as pessimistic as in July, it is difficult to continue to increase the policy and there will be no stronger stimulus policies. Therefore, it is expected that macroeconomic indicators may not be able to improve at the end of the year, and the task of preventing asset bubbles is still relatively difficult. weight.

Exploring the mystery of the divergence of China's economic data

The recent divergence of China's economic data has highlighted the difficulty of judging macroeconomic operations. For example, the main macroeconomic data in July was generally depressed and continued to decline. However, the official manufacturing PMI in August was 50.4, a 22-month high, indicating that the economy is showing signs of improvement. In July, industrial enterprises’ profits rose sharply and power generation was strong. In stark contrast to the sluggish industrial production and investment decline. For example, in July, the profits of industrial enterprises above designated size increased by 11% year-on-year, and the growth rate was 5.9 percentage points faster than that in June. The year-on-year growth rate of power generation increased from 2.1% in June to 7.2%, but the added value of industrial enterprises above designated size increased by 6%. It continued to fall by 0.2 percentage points from June. From January to July, the fixed assets investment decreased to 8.1% year-on-year, which was 0.9% lower than that in January-June. Under the background of the steady growth policy, the investment went down all the way, and the data divergence deserved attention.

What is the logical chain behind the fog? Is the economic situation stable or persistently depressed?

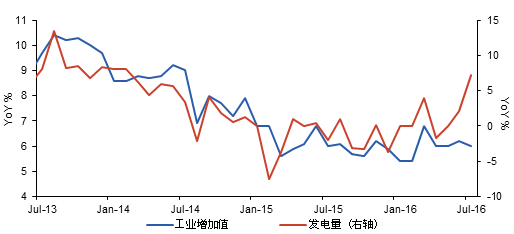

Industrial production declines and power generation and profit growth deviate

One aspect that deserves attention is the mystery of the decline in industrial value added and the strong power generation and the increase in profits. The data shows that the industrial added value of industrial enterprises above designated size increased by 6% year-on-year in July, and the growth rate dropped by 0.2 percentage points from June. However, in July, the profits of industrial enterprises above designated size increased by 11% year-on-year, and the growth rate was 5.9 percentage points faster than that in June, a record high in four months; the power generation and electricity consumption increased sharply, and the power generation increased from 2.1 in June. % rose to 7.2%, and electricity consumption and growth rate rose from 2.6% in June to 8.2%.

Figure 1: Deviation from industrial production and power generation data

In general, there is a high positive correlation between power generation and industrial production, and this directional deviation is anomalous. For this phenomenon, the statistics bureau gave three reasons for explanation: first, the increase in electricity consumption caused by high temperature and heat, second, the short-term adverse impact of flood disasters on industrial production, and third, the low base of industrial electricity consumption. However, in my opinion, the above three explanations and data still have deviations, and the explanatory power is weak. The first reason is that the heat is used to increase electricity consumption. It is true that high temperature will have a greater impact on residential electricity and service industry electricity consumption. For this reason, the growth rate of urban and rural residents' electricity consumption in July accelerated from 5.4% in June to 9.6%, and the tertiary industry's power consumption increased year-on-year. The rate accelerated by 15.3% from 8% in June. However, since the electricity consumption of residents and the tertiary industry account for only 25.6% of the total electricity consumption, the electricity consumption increased by residents and the tertiary industry due to high temperature only contributed 1.5 percentage points to the increase in total electricity consumption. It is difficult to simply attribute the increase of 5.6 percentage points in electricity consumption to this.

Of course, some explanations suggest that there is also a high temperature factor in the increase in electricity consumption in the secondary industry. For example, the year-on-year growth rate of electricity consumption in the secondary industry has accelerated from 1.4% in June to 6.9%, of which industrial electricity consumption has increased from 1.4%. Accelerated to 6.9%, manufacturing power consumption growth accelerated from 0.5% to 4.9%. However, the author believes that it is not possible to attribute the increase in electricity consumption in the above secondary industries to high temperatures. After all, compared with the previous years, it can be found that July 2010 was the highest temperature in the same period of recent years, but the electricity consumption of the secondary industry in 2010 This is obviously different from this year. The growth rate in July slowed down from 15.8% in June to 15.4%, of which the growth rate of industrial electricity consumption slowed from 15.7% to 15.4%, and the growth rate of manufacturing electricity consumption was 19.8%. Slowed down to 15.7%.

The second reason is that floods in some areas have had a certain impact on industrial production. However, according to the analysis of industrial production in the affected provinces, it was found that the disaster situation of the provinces and the deceleration of industrial production did not match exactly. For example, according to the July disaster analysis report released by the Ministry of Civil Affairs, Hebei, Hubei, Anhui, and Henan suffered heavy losses, while the industrial growth in these four provinces only slightly slowed down, 5.1%, 8.3%, and 7.7% respectively. 7.6%, down 0.1, 0, 1.4 and 0.6 percentage points from June. In Hunan, Guizhou, Jiangxi, Jilin, Beijing, Sichuan and other disaster-stricken areas, the growth rate of industrial added value in July was even higher than that in June. The provinces with the largest deceleration rate are not affected by the disaster areas. For example, the industrial added value of Xinjiang, Tibet, and Hainan decreased by 7, 4.5, and 2.6 percentage points respectively in July, which cannot be explained by the negative impact of flood disasters.

Chart 2: The decline in industrial production growth in the affected areas is not significant

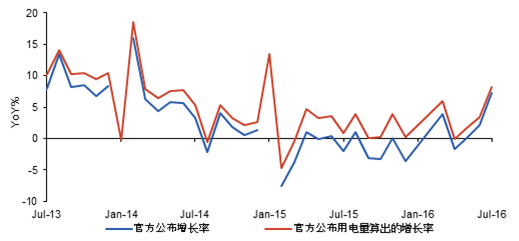

The third reason is the cardinal effect. According to the statistics of the Bureau of Statistics, power generation in July last year slowed down by 2.02%. But is it because of the low base effect that led to a large increase in power generation in July this year? The author still has doubts. According to the Energy Bureau, when the power generation in July 2015 was 509 billion, the power generation in July 2014 was 505 billion kWh. According to this calculation, the growth rate increased by 0.8% year-on-year. -2.02% exists in and out. Of course, data that may be seasonally adjusted, but lacking transparency, may inevitably raise questions about the interpretation of low cardinal effects.

Figure 3: Officially announced the gap between the growth rate of electricity consumption and the absolute value

In addition, from the industry data, among the 27 industries, the growth rate of industrial added value of 18 industries has increased, and the production and sales of emerging products in the direction of consumption upgrading are booming. For example, from January to July, new energy vehicles increased by 94.6% year-on-year, sports multi-purpose passenger vehicles (SUVs) increased by 37.7%, carbon fiber reinforced composite materials increased by 36.7%, solar cells increased by 26.4%, industrial robots increased by 27.2%, mobile phones The growth was 23.8% and the fiber growth was 31.3%. At the same time, the growth of high value-added industries is good. From January to July, radar and ancillary equipment manufacturing increased by 61.5% year-on-year, tram manufacturing increased by 39%, aerospace equipment and equipment manufacturing increased by 24.2%, nuclear radiation processing increased by 18.8%, communications equipment manufacturing increased by 18.5%, and nuclear fuel processing increased by 16.1%. Battery manufacturing increased by 16%. The continued decline in investment should eliminate the impact of abnormal samples in Liaoning

In addition, the continued decline in fixed asset investment continues to differ from the current steady growth policy. Data show that fixed asset investment dropped significantly in July, with a cumulative year-on-year decrease of 8.1% from 9% in June, the fastest growth rate since 1999. However, the author finds that the current fixed asset investment data is actually largely distorted by the unusually large drop in Liaoning Province.

For example, in the first half of this year, Liaoning's accumulated fixed asset investment fell by 58.1% year-on-year. Compared with the financial crisis, Liaoning's fixed asset investment once reached a growth rate of 60%. Liaoning fixed asset investment data has appeared in the cliff since 2015. The decline. The reasons for this are the factors of its own economic downturn, and the reasons for the squeezing of statistics. For example, the proportion of fixed capital formation and fixed asset investment in Liaoning Province to GDP has been highly consistent before 2006, but the gap has gradually widened in 2008-2014. After 2014, the gap between the two has gradually narrowed, and fixed asset investment data. Abnormal fluctuations cause problems in analyzing the real situation of investment.

Chart 4: The decline in fixed asset investment in Liaoning Province since 2015

In contrast, in addition to Liaoning Province, the fixed asset investment of other provinces this year has rebounded in the context of the fiscal stimulus of local governments. From the overall situation of the country, the abnormal sample data of Liaoning disturbed the overall trend of other provinces and cities. After eliminating the significant negative growth in Liaoning Province, the national fixed asset investment (except Liaoning Province) remained relatively stable in the second quarter. From this perspective, The current fixed asset investment data or the steady growth measures have shown signs of stabilization.

Figure 5: National fixed asset investment (except Liaoning Province) is relatively stable

Low credit data also needs to consider the impact of debt swap In addition, the July credit data is also worthy of attention. In July, RMB loans increased by 463.6 billion yuan, a year-on-year increase of 1.01 trillion yuan. Among them, non-financial enterprises and government group loans decreased by 2.6 billion yuan, and household sector loans increased by 457.5 billion yuan. According to this data, there is almost no credit demand in the current real economy, indicating that economic activity is very weak. But in fact, the author believes that the interpretation of credit data also needs to consider the impact of government debt swaps. This year, the government's debt swaps exceeded 5 trillion, and the monthly average also has 4,000-5,000 trillion, and the monthly replacement quota fluctuates greatly. Considering the impact of local government debt swaps on monthly credit data, it is expected that the credit situation in July may not be as negative as the negative growth.

Exhibit 6: New loans in July ignore the impact of debt swaps

In summary, the author believes that when analyzing current Chinese economic data, it is necessary to combine multiple data to make an interpretation. For example, when considering actual industrial production, industrial added value data has a directional deviation from power generation data and industrial enterprise profits. From the data point of view, the positive factors in the operation of industrial economy have increased, and the fundamentals of new kinetic energy accelerating accumulation have not changed. The added value of the high-end segment industry still maintains a relatively high growth rate, and the actual industrial production situation is not as pessimistic as the industrial value-added data that continues to decline. Similarly, the current investment and credit data may be slightly better than the actual data, after removing the national fixed asset investment after the abnormal sample data of Liaoning and considering the credit data under the debt replacement factor. From this perspective, the current economic operation is not as pessimistic as the industrial added value and investment data show, which can be seen from the rebound in August PMI. However, the risks cannot be underestimated. On the one hand, economic structural problems are still outstanding. Real estate first- and second-tier cities are extremely hot, house prices continue to rise, and there is a crowding out effect on the real economy. In the second half of the year, the Fed raises interest rates and increases the pressure on capital outflows and exchange rate depreciation.

On the other hand, the space for policy is decreasing. In July, the fiscal general expenditure increased sharply from 20% in June to 0.3%. The growth rate of M2 dropped from 11.8% in June to 10.2%. New RMB loans fell 68.7% year-on-year. The fiscal, monetary and credit sectors weakened. It is also an important reason for the decline in economic data in July.

In the second half of the year, considering the monetary policy, due to the risks of the real estate market and financial market, there are also expectations of the Fed’s interest rate hike and RMB depreciation and capital outflows. The monetary policy is not as loose as the first half of the year. The interest rate cut will continue to be based on targeted support. In terms of fiscal policy, this year's fiscal expenditure is relatively early. The rare deficit in the first half of the year indicates that space is limited in the second half of the year. In July, the national fiscal general expenditure increased by only 0.3% year-on-year, while the central level fell by 7.4%. It is a sign.

In short, the author believes that although China's current economic data is not as pessimistic as in July, it is difficult to continue to increase the policy, and there will be no stronger stimulus policies. Therefore, it is expected that various macroeconomic indicators may not be able to improve at the end of the year to prevent assets. The task of the bubble is still heavy. In this context, speeding up supply-side reforms, accelerating reforms in terms of dissolving excess capacity, dealing with zombie enterprises, relying on market forces to promote fair competition among state-owned enterprises and private enterprises, reducing administrative approvals, promoting urbanization strategies, and improving social security for residents are Avoid the trap of middle income and regain the inevitable demand for economic growth.

(The author of this article: Ph.D. in Economics, currently Managing Director of Mizuho Securities Asia, Chief Economist. Visiting Professor of School of Economics, Fudan University, member of the 50-member Forum of China New Supply Economics.)

Air Blower,Gas Blower ,Lawn Blower,Garden Blower

Ebic Tools Limited , http://www.ebictools.com